- Delphi general FAQs

- FAQs Why some Delphi salaried retirees will receive payments from both PBGC and Prudential (2013)

- Delphi FAQs for benefit impacts from PBGC sale (2011)

- Important tax information for participants in Delphi’s Salaried Employees Plan (2010)

- Delphi Corporation plan history

- Delphi news releases

FAQs Why some Delphi salaried retirees will receive payments from both PBGC and Prudential (2013)

Starting June 1, 2013, about 6,000 Delphi salaried retirees will see a change in how they receive their retirement benefit. They will continue to receive the same benefit amount.

If you are one of the affected retirees, PBGC sent you a letter on April 30, 2013. The letter explains that instead of a single monthly benefit payment, you will now receive two payments each month.

You will continue to receive a monthly payment from PBGC. The amount will be lower than the payment you currently receive from us. You will also receive a second payment each month from Prudential Insurance Company of America.

Added together, the two benefit payments equal the total monthly amount you have been receiving.

The average monthly amount that Prudential will be paying is $46. Our letter tells you the specific amounts you will receive from PBGC and from Prudential.

Seventy-six former Delphi salaried workers who have not yet begun to receive their pension benefit are also affected by this change. We have sent them a letter to explain how they should apply for their benefit from PBGC and from Prudential.

A: After PBGC took responsibility for your Delphi pension benefit in 2009, we learned that your benefit had been funded by two separate sources. Most of your benefit was funded by Delphi. However, a small portion was funded by your employee contributions. Your pension plan used your contributions to purchase an annuity for you from an insurance company. This small annuity will now be paid by Prudential.

A: PBGC has been working for several years with Prudential and the other insurers involved (Aetna Life Insurance Company and Metropolitan Life Insurance Company) on this long, complex process. We now have an agreement with the insurers to have Prudential pay the annuities. We wanted to ensure a smooth transition with minimal impact on you and the other retirees.

A: Your annuity was purchased long before PBGC became responsible for your pension plan. It is separate from the benefit that PBGC pays. The insurance company has an irrevocable commitment to pay the annuity.

A: Sorry, but no. The insurers are responsible for paying the annuity. PBGC can't keep paying it.

A: The annuities were actually sold by all three companies. However to keep it simple, Prudential is acting as the lead administrator and will pay your annuity on behalf of the three insurers.

A: The annuities were purchased by General Motors before 2000. When Delphi was spun off from General Motors, the annuities were transferred to the Delphi Retirement Program for Salaried Employees, effective May 1, 2000.

A: We can't speak for Prudential on that issue. Please contact them at 1-800-621-1089 for an answer to your question.

A: No. For purposes of the limit, your total benefit continues to include the annuity amount. If your benefit was reduced because of the congressional limits, it will not change.

A: Yes. Since you'll be getting paid by both organizations, you will have to contact them both.

The best way to keep in touch with PBGC is through our online service, MyPBA. Also, you can call us Monday through Friday, 8 a.m.-7 p.m. ET at 1-800-400-7242.

Prudential's telephone number is 1-800-621-1089.

A: You will have to apply with both PBGC and Prudential.

The easiest way to apply for your PBGC benefit is through our secure online service, MyPBA. You should fill out your application no sooner than four months before you want to start benefits. To start receiving your annuity payment from Prudential, call 1-800-621-1089.

A: No, if you haven't yet retired, you can start getting your benefit from PBGC at the same time as your annuity from Prudential, or on a different date. It's up to you. Also, you don't have to choose the same form of annuity for both benefits.

A: While PBGC is pleased with this transaction, the dollars we will receive are less than 10% of the amount that we need to fund the benefits. PBGC doesn't know how this action will affect benefits.

A: Most participants will receive their full benefit because the benefit they were entitled to at the time their plan terminated was smaller than the amount that PBGC guarantees. A pension plan’s assets only come into play when the benefit you earned under the plan is larger than what PBGC guarantees. If you are receiving your full benefit, this transaction will have no effect on your benefit.

A: The most likely group to be helped by the additional money is those who retired or could have retired by July 31, 2006, 3 years before the plan ended. This is because any additional monies PBGC receives will go first to these participants. However, because the amount we will receive is such a small percentage of what PBGC needs to pay benefits, any benefit increases to these participants will be very small.

Important tax information for participants in Delphi’s Salaried Employees Plan (2010)

Important Information

The Delphi Salaried Plan (the Plan) allowed eligible participants to make after-tax contributions from their paychecks to increase their retirement benefits. PBGC does not report the taxable amount of your annuity payments to the Internal Revenue Service, only the total or gross amount paid. If you made after-tax employee contributions to the Plan you will need to determine the portion of your PBGC monthly benefit that is considered taxable income for your 2010 Federal Income Tax Return.

A: Based on information we received from the plan, all of your annuity payments are taxable income. The Plan treated your employee contributions as being in a separate pension plan for tax reporting purposes. Therefore, when you withdrew your contributions, the withdrawal was treated as a total distribution of that plan’s benefit, and the entire amount of your contributions was treated as non-taxable income when they were paid to you. As a result, the Plan subsequently treated your annuity payments as provided entirely by the employer and thus as fully taxable.

The amount in Box 1, Gross distribution, of your 1099-R from PBGC for 2010 should be the taxable amount of your annuity.

A: If you did not withdraw your contributions, your annuity payments include a benefit provided by your employee contributions. Therefore, a portion of your annuity payments are non-taxable and you must determine the taxable amount of your annuity payments. The Plan would have computed the non-taxable and taxable amounts of your annuity payments when you retired. The non-taxable amount of your annuity payments would have first been computed as a monthly amount. This monthly amount generally remains the same, even if the amount of your payments later changed.

You should be able to determine the non-taxable and taxable amounts of your annuity payments using information from 1099-R's you received from the Plan for years before PBGC began making payments to you (1099-R's for 2009 and earlier) and information from the 1099-R that PBGC to sent you for 2010.

- Non-taxable amount of payments. To determine the monthly non-taxable amount:

- Subtract the amount in Box 2a, Taxable income, of the 1099-R from the plan, from the amount in Box 1, Gross distribution, of the 1099-R from the plan.

- Divide the difference by 12 months.

- If the amount previously reported was for more or less than 12 months of payments, you will need to divide by the actual number of months for which payment was received (for example, you retired in the middle of 2009 and only received payments for 6 months).

- Taxable amount of PBGC payments. To determine the taxable amount of your annuity payments from PBGC:

- Multiply the monthly non-taxable amount (from above) by the number of months for which you received payments in 2010. In most cases, this will be 12 months.

- Subtract that non-taxable amount from the amount in Box 1, Gross distribution, of your 1099-R for 2010 from PBGC.

- Taxable amount of future payments. The monthly non-taxable amount will remain the same, even if your payments from PBGC change. This portion of your annuity payments remains non-taxable in order to recover all your contributions tax-free. You should have received information showing the total contributions (without interest) that you should recover tax-free from the Plan when you retired.

Example

- From your 1099-R for 2009 from the Plan:

- Box 1, Gross distribution: $25,000

- Box 2a, Taxable Amount: $24,160

- The difference in Box 1 and Box 2a: $840 ($25,000 - $24,160)

- Number of months you received payments for in 2009: 12

- Monthly non-taxable amount of your annuity payments: $70 ($840 ÷ 12)

- From your 1099-R for 2010 from PBGC, Box 1, Gross distribution: $23,000

- Number of months you received payments for in 2010: 12

- Non-taxable amount of annuity payments for 2010: $840 ($70 X 12)

- Taxable amount of annuity payments for 2010: $22,160 ($23,000 - $840)

A: We suggest that you follow the instructions in IRS Form 1040 and its instructions (1040 Instructions) which can be found at www.irs.gov to determine the non-taxable and taxable amounts of your annuity. In addition, IRS Publication 575 Pension and Annuity Income (For use in preparing 2010 Returns) provides additional information. Both publications include information about the Simplified Method, which is used to determine the non-taxable and taxable amounts of a monthly annuity payment, and provide worksheets that can be used to compute the taxable amount of your annuity payments for 2010. You will need information from documents we have already sent to you to do this computation.

A: You should have already received the following documents from PBGC:

- Form(s) 1099-R for 2010 issued by PBGC’s paying agent, State Street Corporation.

You may have received more than one 1099-R from PBGC; for example, if you began receiving for your annuity payments, and withdrew your employee contributions in a single sum and/or if you received a larger back payment of your annuity payments in a single sum of $5,000 or more.

- PBGC Benefit Estimation

- 503MEC Letter, if you withdrew your employee contributions in a single sum from PBGC.

If you do not have these documents, please contact us for a copy.

A:

1099-R for annuity payments.You will need the amount in Box 1, Gross distribution from the 1099-R for your annuity payments.

1099-R for non-periodic payments. If you also received a 1099-R for a non-periodic or single-sum payment, for example, a withdrawal of your contributions or a large back payment of annuity payments, you will need the amount in Box 2a. Taxable amount.

Box 5. Employee contributions on the 1099-R may have an entry, which is the amount of the payment that was non-taxable. This amount should be the same as the amount shown in your 503MEC Letter as the "Estimated nontaxable amount" if you received one (see Question 3d). Let us know if these amounts are different.

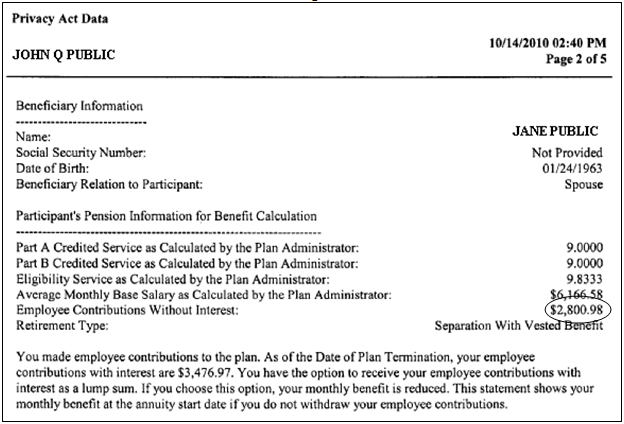

A: Your PBGC Benefit Estimation provides your "Employee Contributions without Interest" as of the date of plan termination, July 31, 2009. It may also contain additional information if you made any withdrawals before the plan terminated. Image A below shows where this information appears (circled):

Image A

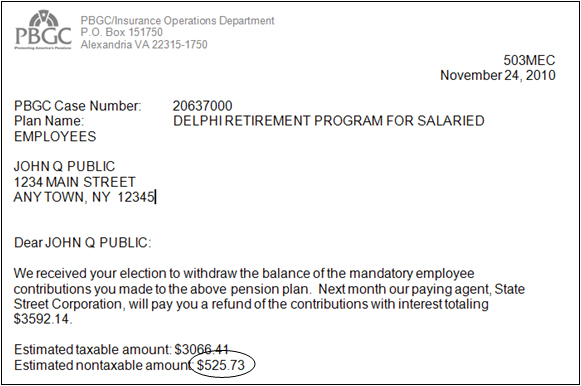

A: The 503MEC Letter sent to you by PBGC provides the "Estimated nontaxable amount" of your withdrawal. This amount should be the same as the amount shown in Box 5. Employee contributions of your 1099-R for the withdrawal (see Question 3b). Let us know if these amounts are different. Image B below shows where this information appears on the 503MEC Letter (circled):

Image B

Please note that the difference between your "employee contributions with interest" shown on your PBGC Benefit Estimation and the "refund of the employee contributions with interest" on your 503MEC Letter is additional interest we paid you from the date the plan terminated, July 31, 2009, to the date your employee contributions were paid.

A: As Worksheet A suggests, you should refer to Cost (Investment in the Contract) for detailed instructions on how to determine your cost in the plan.

Generally, your cost in the plan is the difference between the actual amount of employee contributions you made minus the non-taxable amount of any contributions that you may have withdrawn before or at the time you retired. The following example refers to the PBGC Benefit Estimation (Image A) and 503MEC letter (Image B), above:

Example:

|

Employee Contributions without Interest |

Estimated non-taxable amount of withdrawal (Image B) |

|

|---|---|---|

|

$2800.98 |

$525.73 |

$2275.25 |

The net cost in the plan is entered on Line 2 of Worksheet A, as follows:

IRS Publication 575, Worksheet A, Simplified Method, Line 2:

A: Your cost in the plan is your "Employee Contributions without Interest" as of July 31, 2009, as shown in your PBGC Benefit Estimation (Image A).

A: PBGC realizes that tax information can be complicated and difficult to understand. Sources of additional tax information and guidance that you may find helpful, include:

- IRS Publication 575 Pension and Annuity Income (For use in preparing 2010 Returns), which can be found on the IRS website.

- IRS Form 1040 and its instructions (1040 Instructions), which can also be found on the IRS website.

- Internal Revenue ServiceThe IRS provides help for tax questions in several ways, many of them free. These are listed in IRS Publication 575 and on the IRS website.

We also suggest that you check with your own tax consultant. And of course, please do not hesitate to contact our Customer Contact Center at 1-800-400-7242 for help.