I. Introduction

Plan administrators of certain underfunded plans must notify participants and beneficiaries annually of the plan's funding status and the limits of the PBGC's guarantee. See ERISA section 4011 and 29 CFR Part 4011.

The PBGC regulation implementing ERISA section 4011 includes a Model Participant Notice that plan administrators may use to meet the Participant Notice requirement. For the convenience of plan administrators, each year the PBGC republishes the Model Participant Notice, updated to reflect the latest information on maximum guaranteed benefits.

A detailed description of the rules governing the requirement to issue a 2004 Participant Notice is contained in section III below. As in prior years, this Technical Update also includes a Worksheet to help plan administrators determine whether they must issue a 2004 Participant Notice.

Plan administrators of most new and newly-covered plans are exempt from the Participant Notice requirement. Plan administrators of small plans are NOT exempt from the Participant Notice requirement. However, there are special rules that allow plan administrators of small plans to avoid doing additional calculations by using numbers already reported on Schedule B to the Form 5500. A plan administrator may issue a Participant Notice even if it is not required.

This Technical Update explains how the interest rate changes enacted by the Job Creation and Worker Assistance Act of 2002 ("JCWAA") and the Pension Funding Equity Act of 2004 ("PFEA") can affect the requirement to issue a 2004 Participant Notice (discussed in section III below) or the plan funding information required to be disclosed in a 2004 Participant Notice (discussed in section IV below).

II. Due Dates

A 2004 Participant Notice is due two months after the due date (including extensions) for the 2003 Form 5500. Due dates that fall on a weekend or Federal holiday are extended to the next business day. The following table shows the common due dates for calendar year plans:

|

2003 Form 5500 |

2004 Participant Notice |

|---|---|

|

Monday, August 2, 2004 |

Monday, October 4, 2004 |

|

Wednesday, September 15, 2004 |

Monday, November 15, 2004 |

|

Friday, October 15, 2004 |

Wednesday, December 15, 2004 |

Participant Notice Voluntary Correction Program - Reminder

The Participant Notice Voluntary Correction Program ("VCP"), announced May 7, 2004, in the Federal Register (69 Fed. Reg. 25792), covers any 2002 or 2003 Participant Notice: (1) that was due (without regard to any deadline extension resulting from a disaster relief notice) before May 7, 2004; and (2) that was not, as of May 7, 2004, the subject of a PBGC audit proceeding. Under the VCP, the PBGC will not assess a penalty for a 2002 or 2003 Participant Notice failure if the plan administrator corrects the failure in accordance with the VCP guidelines. In addition, the PBGC will not pursue any failure to provide a pre-2002 Participant Notice unless there is a 2002 or 2003 Participant Notice failure that is covered by the VCP but that does not meet the requirements for penalty relief under the VCP.

The PBGC anticipates that many plan administrators will want to participate in the VCP as a precaution, even in the absence of a known Participant Notice failure. Participation in the VCP will not affect the likelihood that a plan will be selected for audit of compliance with the Participant Notice requirement for a post-VCP plan year, the PBGC premium requirement for any plan year, or any other PBGC requirement. Complete information on the VCP (including a model VCP corrective notice) and on the Participant Notice requirements can be found on the PBGC's Web site.

Note: The VCP is a one-time chance to "wipe the slate clean" - without any penalty - before the PBGC steps up its enforcement of the Participant Notice requirement. The deadline for taking advantage of this program depends on the plan's Form 5500 deadline for the 2003 plan year, and may be as early as October 4, 2004. The 2004 Model Participant Notice includes instructions about VCP requirements for those plan administrators who are participating in the VCP.

This Technical Update uses the following terms:

FCL Percentage - A plan's Funded Current Liability Percentage obtained by dividing:

- The actuarial value of the plan's assets (not reduced by any credit balance in the funding standard account), determined as of the plan's valuation date

by

- The plan's current liability determined using the applicable interest rate (as specified in the Interest Rate Table for 2004 Plan Year, below) for the plan year, determined as of the plan's valuation date.

An alternate method for determining a plan's FCL Percentage is available for small plans - see Special Small Plan Rules in Section V below.

PFEA Optional Recalculation - An optional recalculation of a plan's FCL Percentage for plan years beginning in 2001, 2002, or 2003 solely to determine whether the plan meets the DRC Exception Test (see below) for the 2004 plan year, as permitted under PFEA § 101(d)(3).

100% Weighted Corporate Rate - 100% of the weighted average of the annual rate of interest determined by the Secretary of the Treasury on amounts invested conservatively in long-term investment grade corporate bonds. This rate applies for calculating current liability for plan years beginning in 2004 or 2005 and for certain prior plan years under the PFEA Optional Recalculation rule.

120% Weighted Treasury Rate - 120% of the weighted average of the yield on 30-year Treasury securities. This rate applies for calculating current liability for plan years beginning in 2002 or 2003.

105% Weighted Treasury Rate - 105% of the weighted average of the yield on 30-year Treasury securities. This rate applies for calculating current liability for plan years beginning in 1999, 2000, or 2001.

These rates are published monthly by the Internal Revenue Service. A summary of the rates that might be needed to determine if a 2004 Participant Notice is required is included as an appendix to this Technical Update.

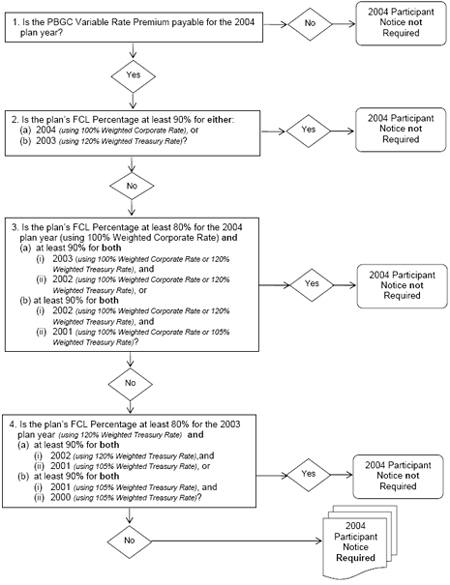

III. Requirement to Issue a 2004 Participant Notice

The plan administrator of any single-employer plan for which a variable rate premium ("VRP") is payable for the 2004 plan year is required to issue a 2004 Participant Notice, unless the plan meets a funding-related test tied to the "deficit reduction contribution" rules - the "Deficit Reduction Contribution ("DRC") Exception Test" (discussed below) - for the 2004 plan year or the 2003 plan year.

Thus, a plan administrator is required to issue a 2004 Participant Notice unless the plan meets one of the following three criteria:

- No VRP is payable for the 2004 plan year,1

- The plan meets the DRC Exception Test for the 2004 plan year, or

- The plan meets the DRC Exception Test for the 2003 plan year.

VRP

A plan administrator is not required to issue a 2004 Participant Notice if a VRP is not payable for that plan year, either because (1) the plan has no unfunded vested benefits (determined on a premium basis), or (2) because the plan qualifies for at least one of five exemptions from the VRP contained in the PBGC's regulation on Premium Rates. One of these exemptions is for plans at the full funding limit (FFL) under 29 CFR § 4006.5(a)(5).

The 2003 FFL required to be reported on the 2003 Form 5500, Schedule B, is used to determine whether the plan qualifies for the full funding limit exemption from the VRP for the 2004 plan year, based on contributions for the 2003 plan year.

The PFEA Optional Recalculation rule does not apply in this context.

DRC Exception Test

A plan administrator is not required to issue a 2004 Participant Notice if the plan meets the DRC Exception Test for either the 2004 or 2003 plan year. Whether a plan meets the DRC Exception Test for a plan year depends on whether the plan's FCL Percentage is at or above various specified levels for several plan years. Specifically -

- A plan meets the DRC Exception Test for the 2004 plan year if the plan's FCL Percentage -

- Is at least 90% for the 2004 plan year, or

- Is least 80% for the 2004 plan year and at least 90% for either -

- The 2003 plan year and the 2002 plan year, or

- The 2002 plan year and the 2001 plan year.

- A plan meets the DRC Exception Test for the 2003 plan year if the plan's FCL Percentage -

- Is at least 90% for the 2003 plan year, or

- Is least 80% for the 2003 plan year and at least 90% for either -

- The 2002 plan year and the 2001 plan year, or

- The 2001 plan year and the 2000 plan year.

Participant Notice Worksheet

Determining whether a Participant Notice is required for the 2004 plan year can be more complex than for past plan years. Three different interest rate bases can apply for determining the plan's FCL Percentage for the five years 2000 through 2005. In some cases plan administrators have the option of recalculating previous determinations of FCL Percentages using a higher interest rate under the PFEA Optional Recalculation rule. Thus, plan administrators are encouraged to use the Worksheet, paying particular attention to the various interest rates required or permitted to be used in determining the plan's FCL Percentage for each plan year.

The Worksheet presents one order of steps for determining whether a 2004 Participant Notice is required. However, a plan administrator may wish to use a different order, particularly if a plan's FCL Percentages reported on prior Forms 5500, Schedule B, may be sufficient to satisfy the DRC Exception Test for the 2004 or 2003 plan years.

PFEA Optional Recalculation

In general, a plan's FCL Percentages for plan years prior to the 2004 plan year have been reported on prior Forms 5500, Schedule B. In many cases, the FCL Percentages calculated for one or more prior plan years will be sufficiently high that the plan meets the DRC Exception Test for the 2004 plan year or the 2003 plan year.

If the plan does not meet the DRC Exception Test for 2004 or 2003 using the FCL Percentages that were originally calculated, the plan may recalculate the FCL Percentages under the PFEA Optional Recalculation rule for the 2004 DRC Exception Test. Under this rule, the FCL Percentages for the 2001, 2002, and 2003 plan years may be recalculated using the 100% Weighted Corporate Rate. Note that the PFEA Optional Recalculation will always result in a higher FCL Percentage than the FCL Percentage previously calculated (see Interest Rate Table).

The PFEA Optional Recalculation rule is not applicable to the DRC Exception Test for the 2003 plan year. Thus, the FCL Percentages for the 2001 through 2003 plan years used to determine whether the plan meets the DRC Exception Test for the 2004 plan year might be different from the FCL Percentages for the 2001 through 2003 plan years used to determine whether the plan meets the DRC Exception Test for the 2003 plan year.

The following table provides a summary of which interest rate(s) must be used to determine if a Participant Notice is required for the 2004 plan year.

|

FCL Percentage |

2003 DRC Exception Test |

2004 DRC Exception Test |

|---|---|---|

|

2004 plan year |

N/A |

100% Weighted Corporate Rate |

|

2003 plan year |

120% Weighted |

120% Weighted Treasury Rate, |

|

2002 plan year |

120% Weighted |

120% Weighted Treasury Rate, |

|

2001 plan year |

105% Weighted |

105% Weighted Treasury Rate, |

|

2000 plan year |

105% Weighted |

N/A |

![]() Examples

Examples

The following examples show how the Worksheet is used to determine whether a 2004 Participant Notice is required.

Example 1. A VRP is payable for Plan A for the 2004 plan year. Therefore, the plan administrator of Plan A is required to issue a 2004 Participant Notice unless the plan meets the DRC Exception Test for the 2004 plan year or for the 2003 plan year. The following chart summarizes Plan A's FCL Percentages for relevant plan years:

|

Plan Year |

100% Weighted Corporate Rate |

120% Weighted Treasury Rate |

105% Weighted Treasury Rate |

|---|---|---|---|

|

2004 |

85% |

N/A |

N/A |

|

2003 |

75% |

70% |

N/A |

|

2002 |

89% |

91% |

N/A |

|

2001 |

91% |

N/A |

80% |

|

2000 |

N/A |

N/A |

79% |

Following the steps in the Worksheet:

- Is a VRP payable for the 2004 plan year?

Yes. - Is the plan's FCL Percentage at least 90% for either the 2004 plan year (determined using the 100% Weighted Corporate Rate) or the 2003 plan year (determined using the 120% Weighted Treasury Rate)?

No. The plan's FCL Percentage for the 2004 plan year is 85% (determined using the 100% Weighted Corporate Rate). The plan's FCL Percentage for the 2003 plan year is 70% (as previously reported on Schedule B, determined using the 120% Weighted Treasury Rate). -

Is the plan's FCL Percentage at least 80% for the 2004 plan year (determined using the 100% Weighted Corporate Rate) and

- at least 90% for both

- the 2003 plan year (determined using the 100% Weighted Corporate Rate or the 120% Weighted Treasury Rate) and

- the 2002 plan year (determined using the 100% Weighted Corporate Rate or the 120% Weighted Treasury Rate) OR

- at least 90% for both

- the 2002 plan year (determined using the 100% Weighted Corporate Rate or the 120% Weighted Treasury Rate) and

- the 2001 plan year (determined using the 100% Weighted Corporate Rate or the 105% Weighted Treasury Rate)?

Yes. The plan's FCL Percentage is 85% for the 2004 plan year (determined using the 100% Weighted Corporate Rate).

Under 3(b), the plan's FCL Percentage for (i) the 2002 plan year is 91% (as previously reported on Schedule B, determined using the 120% Weighted Treasury Rate) and (ii) the 2001 plan year is 91% (determined using the 100% Weighted Corporate Rate, allowed by the PFEA Optional Recalculation rule).

Therefore, the plan administrator of Plan A is not required to issue a 2004 Participant Notice. - at least 90% for both

Example 2. A VRP is payable for Plan B for the 2004 plan year. Therefore, the plan administrator of Plan B is required to issue a 2004 Participant Notice unless the plan meets the DRC Exception Test for the 2004 plan year or for the 2003 plan year. The following chart summarizes Plan B's FCL Percentages for relevant plan years:

|

Plan Year |

100% Weighted Corporate Rate |

120% Weighted Treasury Rate |

105% Weighted Treasury Rate |

|---|---|---|---|

|

2004 |

79% |

N/A |

N/A |

|

2003 |

95% |

81% |

N/A |

|

2002 |

91% |

89% |

N/A |

|

2001 |

95% |

N/A |

85% |

|

2000 |

N/A |

N/A |

85% |

Following the steps in the Worksheet:

- Is a VRP payable for the 2004 plan year?

Yes. - Is the plan's FCL Percentage at least 90% for either the 2004 plan year (determined using the 100% Weighted Corporate Rate) or the 2003 plan year (determined using the 120% Weighted Treasury Rate)?

No. The plan's FCL Percentage is 79% for the 2004 plan year (determined using the 100% Weighted Corporate Rate) and the plan's FCL Percentage is 81% for the 2003 plan year (as previously reported on Schedule B, determined using the 120% Weighted Treasury Rate). - Is the plan's FCL Percentage at least 80% for the 2004 plan year (determined using the 100% Weighted Corporate Rate)?

No. The plan's FCL Percentage is 79% for the 2004 plan year (determined using the 100% Weighted Corporate Rate). - Is the plan's FCL Percentage at least 80% for the 2003 plan year (determined using the 120% Weighted Treasury Rate) and

at least 90% for both

the 2002 plan year (determined using the 120% Weighted Treasury Rate) and

the 2001 plan year (determined using the 105% Weighted Treasury Rate)

OR

at least 90% for both

the 2001 plan year (determined using the 105% Weighted Treasury Rate) and

the 2000 plan year (determined using the 105% Weighted Treasury Rate)?

No. The plan's FCL Percentage is 81% for the 2003 plan year (as previously reported on Schedule B, determined using the 120% Weighted Treasury Rate).

Under 4(a), the plan's FCL Percentage is 89% for (i) the 2002 plan year (as previously reported on Schedule B, determined using the 120% Weighted Treasury Rate) and (ii) 85% for the 2001 plan year (as previously reported on Schedule B, determined using the 105% Weighted Treasury Rate). And under 4(b), the plan's FCL Percentage is (i) 85% for the 2001 plan year (as previously reported on Schedule B, determined using the 105% Weighted Treasury Rate) and (ii) 85% for the 2000 plan year (as previously reported on Schedule B, determined using the 105% Weighted Treasury Rate).

Note: the plan administrator uses the plan's FCL Percentages reported on prior Forms 5500, Schedule B, and cannot use the PFEA Optional Recalculation rule.

Therefore, the plan administrator of Plan B is required to issue a 2004 Participant Notice.

1. A plan administrator may have been required to issue a Participant Notice for the 2002 or 2003 plan year even if a VRP was not payable for that plan year using 100% of the yield on 30-year Treasury securities, but would have been payable for that plan year using 85% of the yield on 30-year Treasury securities. See PBGC Technical Update 04-3. For information on how to correct Participant Notice failures for the 2002 or 2003 plan year without penalty, see Participant Notice Voluntary Correction Program discussed above.

< Back

IV. Funding Information Required to be Disclosed

in a 2004 Participant Notice

A 2004 Participant Notice must disclose the plan's FCL Percentage either:

- For the 2004 plan year, determined using the 100% Weighted Corporate Rate, or

- For the 2003 plan year, determined using the 120% Weighted Treasury Rate.

A plan administrator who is participating in the VCP:

- Must disclose the plan's FCL Percentage for the 2002 and 2003 plan years, both determined using the 120% Weighted Treasury Rate; and

- May also disclose the FCL Percentage for the 2004 plan year, determined using the 100% Weighted Corporate Rate.

V. Special Small Plan Rules

Calculating the Plan's FCL Percentage both for Requirement to Issue a 2004 Participant Notice and for Funding Information Required to be Disclosed in a 2004 Participant Notice

In calculating its FCL Percentage for a plan year, a plan that is a "small plan" (as defined below) for that plan year may use one or both of the following rules:

|

(1) |

|

The plan's FCL Percentage may be calculated by using numbers that are required to be reported on the Form 5500, Schedule B, for the plan year for which the FCL Percentage is calculated. Under this special rule, the FCL Percentage is obtained by dividing - |

The market value of the plan's assets as of the beginning of the plan year

by

The plan's total current liability as of the beginning of the plan year.

|

(2) |

|

When calculating current liability (whether or not the plan uses the special rule in (1) above), if the plan's current liability required to be reported on Form 5500, Schedule B, was calculated using an interest rate lower than the highest allowable interest rate, the current liability at the highest rate may be determined by reducing the reported current liability by one percent for each tenth of a percent by which the highest allowable interest rate exceeds the interest rate used. |

Example: Assume that a small plan's current liability as of January 1, 2004, is $250,000, based on an interest rate of 5.95%. The highest allowable interest rate for the 2004 plan year is 6.55% (the applicable 100% Weighted Corporate Rate). Because the highest allowable interest rate exceeds the interest rate used by six-tenths of a percent, current liability may be reduced by 6% to $235,000, as follows: (1.00 -.06) x $250,000 = $235,000.

Definition of "Small Plan"

A plan is considered to be a "small plan" for a plan year if it had 100 or fewer participants on each day during the preceding plan year. When determining whether a plan is a "small plan," its participants must be aggregated with the participants of all other defined benefit plans maintained by the same employer or any other member of the employer's controlled group in accordance with ERISA section 302(d)(6)(C).

VI. 2004 Participant Notice Worksheet

Note - In some cases, it might be simpler to do step 4 before step 3 (for example, if the 2004 FCL Percentage has not yet been calculated or if you already know the answer to step 4 is "yes" because of analysis done when you determined whether a 2003 Participant Notice was required).

VII. 2004 Model Participant Notice

The following is an example of a 2004 Participant Notice that satisfies the requirements of section 4011.10 when the required information is filled in. Special instructions for plan administrators who are participating in the Participant Notice Voluntary Correction Program ("VCP") are in bold.

NOTICE TO PARTICIPANTS OF [PLAN NAME]

The law requires that you receive information on the funding level of your defined benefit pension plan and the benefits guaranteed by the Pension Benefit Guaranty Corporation (PBGC), a federal insurance agency. [If you are participating in the VCP, you may include a statement to the effect that the plan had a Participant Notice failure for the 2002 plan year or for the 2003 plan year (or for both). You may also include a statement to the effect that the plan is participating in the PBGC's Participant Notice Voluntary Correction Program.]

YOUR PLAN'S FUNDING

[If you are not participating in the VCP, include the following statement.] As of [month/day/year], your plan had [insert Notice Funding Percentage determined in accordance with section 4011.10(c)] percent of the money needed to pay benefits promised to employees and retirees.

[If you are participating in the VCP, include the following two statements (see § 4011.10(c)(2) for special rules small plans may use to determine the plan's funded current liability percentage).]

As of [month/day/year], your plan had [insert plan's funded current liability percentage (as defined in section 302(d)(9)(C) of ERISA) for the 2002 plan year] percent of the money needed to pay benefits promised to employees and retirees.

As of [month/day/year], your plan had [insert plan's funded current liability percentage (as defined in section 302(d)(9)(C) of ERISA) for the 2003 plan year] percent of the money needed to pay benefits promised to employees and retirees.

[If you are participating in the VCP, you may also include the following statement.]

As of [month/day/year], your plan had [insert plan's funded current liability percentage (as defined in section 302(d)(9)(C) of ERISA) for the 2004 plan year] percent of the money needed to pay benefits promised to employees and retirees.

To pay pension benefits, your employer is required to contribute money to the pension plan over a period of years. A plan's funding percentage does not take into consideration the financial strength of the employer. Your employer, by law, must pay for all pension benefits, but your benefits may be at risk if your employer faces a severe financial crisis or is in bankruptcy.

[Include the following paragraph only if, for any of the previous five plan years, the plan has been granted and has not fully repaid a funding waiver.]

Your plan received a funding waiver for [list any of the five previous plan years for which a funding waiver was granted and has not been fully repaid]. If a company is experiencing temporary financial hardship, the Internal Revenue Service may grant a funding waiver that permits the company to delay contributions that fund the pension plan.

[Include the following with respect to any unpaid or late payment that must be disclosed under section 4011.10(b)(6):]

Your plan was required to receive a payment from the employer on [list applicable due date(s)]. That payment [has not been made] [was made on [list applicable payment date(s)]].

PBGC GUARANTEES

When a pension plan terminates without enough money to pay all benefits, the PBGC steps in to pay pension benefits. The PBGC pays most people all pension benefits, but some people may lose certain benefits that are not guaranteed.

The PBGC pays pension benefits up to certain maximum limits.

- The maximum guaranteed benefit is $3,698.86 per month or $44,386.32 per year for a 65 year old person in a plan that terminates in 2004. [If you issue this notice after the maximum guaranteed benefit information for plans that terminate in 2005 is announced, you may add or substitute that information in order to provide participants with more current information. The PBGC expects to make that information available on its web site at www.pbgc.gov in early November 2004.]

- The maximum benefit may be reduced for an individual who is younger than age 65. For example, it is $1,664.49 per month or $19,973.88 per year for an individual who starts receiving benefits at age 55. [In lieu of age 55, you may add or substitute any age(s) relevant under the plan. For example, you may add or substitute the maximum benefit for ages 62 or 60. The maximum benefit is $2,922.10 per month or $35,065.20 per year at age 62; it is $2,404.26 per month or $28,851.12 per year at age 60. If the plan provides for normal retirement before age 65, you must include the normal retirement age.] [If you issue this notice after the maximum guaranteed benefit information for plans that terminate in 2005 is announced, you may add or substitute that information in order to provide participants with more current information. The PBGC expects to make that information available on its web site at www.pbgc.gov in early November 2004.] [If the plan does not provide for commencement of benefits before age 65 you may omit this paragraph.]

- The maximum benefit will also be reduced when a benefit is provided for a survivor.

The PBGC does not guarantee certain types of benefits. [Include the following guarantee limits that apply to the benefits available under your plan.]

- The PBGC does not guarantee benefits for which you do not have a vested right when a plan terminates, usually because you have not worked enough years for the company.

- The PBGC does not guarantee benefits for which you have not met all age, service, or other requirements at the time the plan terminates.

- Benefit increases and new benefits that have been in place for less than a year are not guaranteed. Those that have been in place for less than 5 years are only partly guaranteed.

- Early retirement payments that are greater than payments at normal retirement age may not be guaranteed. For example, a supplemental benefit that stops when you become eligible for Social Security may not be guaranteed.

- Benefits other than pension benefits, such as health insurance, life insurance, death benefits, vacation pay, or severance pay, are not guaranteed.

- The PBGC generally does not pay lump sums exceeding $5,000.

WHERE TO GET MORE INFORMATION

Your plan, [EIN PN], is sponsored by [contributing sponsor(s)]. If you would like more information about the funding of your plan, contact [insert name, title, business address and phone number of individual or entity].

For more information about the PBGC and the benefits it guarantees, you may request a free copy of "Your Guaranteed Pension" by writing to Consumer Information Center, Dept. YGP, Pueblo, Colorado 81009. [The following sentence may be included:] "Your Guaranteed Pension" is also available on the PBGC's Web site at http://www.pbgc.gov.

Issued: [insert at least month and year]